You want to protect your dog or cat from expensive veterinary bills without adding another monthly payment to your budget. The short answer is that 100% free, lifelong pet insurance does not exist. Insurance companies rely on pooled premiums to cover medical payouts, making entirely free lifelong coverage impossible. However, you can access temporary free pet insurance through 30-day trials offered by major providers like Trupanion or AKC. You might also unlock free coverage by adopting from specific shelters or utilizing employer-sponsored benefits where your company covers the premium. Understanding these workarounds, alongside subsidized veterinary alternatives, allows you to secure medical protection for your companion animal without paying standard retail rates.

The Essentials

- Lifelong free coverage is a myth: Traditional pet insurance requires a pooled premium model to pay out claims; therefore, permanent free policies are financially impossible for companies to offer.

- Temporary trials offer genuine protection: You can secure 30 days of actual, zero-premium coverage through promotional certificates offered by breeders, shelters, and major insurers.

- Your employer is your best resource: A growing number of corporate benefits packages now include fully subsidized pet insurance, making the coverage effectively free for the employee.

- Charities bridge the gap: If you face an emergency without insurance, non-profit organizations offer grants to help cover life-saving veterinary care.

Why It Matters Now

The landscape of veterinary medicine looks entirely different today than it did two decades ago. When your dog tears a cranial cruciate ligament—the canine equivalent of an ACL tear—your veterinarian no longer simply prescribes rest and pain medication. Today, the standard of care often involves a highly specialized orthopedic surgery that can easily cost between $5,000 and $10,000 depending on your location. Similarly, treatments for feline hyperthyroidism, canine cancer, and complex gastrointestinal obstructions involve advanced diagnostics like MRIs, CT scans, and targeted chemotherapy.

While this medical advancement means your companion animal can live a longer, healthier life, it also places an enormous financial burden directly onto your shoulders. Unlike human healthcare, where government programs or comprehensive employer plans absorb the shock of catastrophic medical events, veterinary care remains largely an out-of-pocket expense. This harsh reality drives thousands of pet owners to search for free pet insurance every month.

According to data published by the North America Pet Health Insurance Association (NAPHIA), the pet insurance industry exceeded $5.2 billion in total written premiums in North America by the end of 2024, covering over 7 million pets. This explosive growth proves that families are actively seeking financial safety nets. You are part of a massive movement of pet caretakers trying to balance a deep emotional bond with the practical realities of household economics. Knowing that a single emergency visit can wipe out your savings account makes the quest for affordable pet insurance—or the elusive dream of free coverage—more relevant than ever.

How to Get Temporary Free Pet Insurance Coverage

Although you cannot secure a lifelong policy for free, the industry heavily relies on promotional periods to attract new customers. This means you can string together immediate, temporary protection during the highest-risk periods of your pet’s life: the weeks immediately following an adoption or purchase.

When you bring a new puppy or kitten into your home, they face immense stress. They explore their new environment with their mouths, exposing them to foreign object ingestion, dietary indiscretion, and localized infections. To help owners navigate this vulnerable window, major providers partner with shelters, rescue groups, and registered breeders to offer 30-day trial certificates.

Companies like Trupanion and AKC Pet Insurance frequently issue these free trial policies. If you adopt a dog from a participating local shelter, you will likely receive a certificate in your adoption packet. You typically have 24 hours from the time of adoption or the time of your first veterinary examination to activate the coverage. Once activated, the trial functions exactly like a paid pet insurance coverage plan for 30 days. It protects your animal against sudden accidents and new illnesses, minus a pre-determined deductible.

You pay zero premiums during this month. If your newly adopted cat develops an upper respiratory infection on day fourteen, you simply pay the deductible, and the temporary insurance covers the remaining eligible vet bill. At the end of the 30 days, the coverage automatically drops unless you choose to provide your credit card information and convert it into a standard paid policy.

“Keep your sleeping cat healthy with employer-sponsored pet insurance while working from home.”

Employer-Sponsored Pet Health Insurance

If you want permanent free pet insurance, your workplace represents your single best opportunity. Over the last few years, companies have recognized that modern employees view their pets as direct family members. To remain competitive in the labor market and retain top talent, human resources departments have increasingly added pet health insurance to their standard benefits packages.

Employer-sponsored pet insurance generally falls into two distinct categories. The first is a voluntary benefit structure. In this scenario, the employer negotiates a group discount rate with a major insurance provider. You still pay the monthly premium out of your paycheck, but the cost is significantly lower than what you would find on the open consumer market. While helpful, this is simply affordable pet insurance rather than free coverage.

The second category is fully subsidized coverage. A growing number of progressive corporations now treat pet insurance exactly like human dental or vision care. The employer pays 100 percent of the base monthly premium for one or sometimes multiple pets. For the employee, this translates into genuinely free pet insurance plans. You remain responsible for co-pays and deductibles when your animal actually needs medical care, but the recurring monthly premium burden vanishes entirely. If you are currently job hunting or navigating open enrollment at your current company, reviewing the pet benefits section could save you hundreds of dollars annually.

The Real Cost of Affordable Pet Insurance

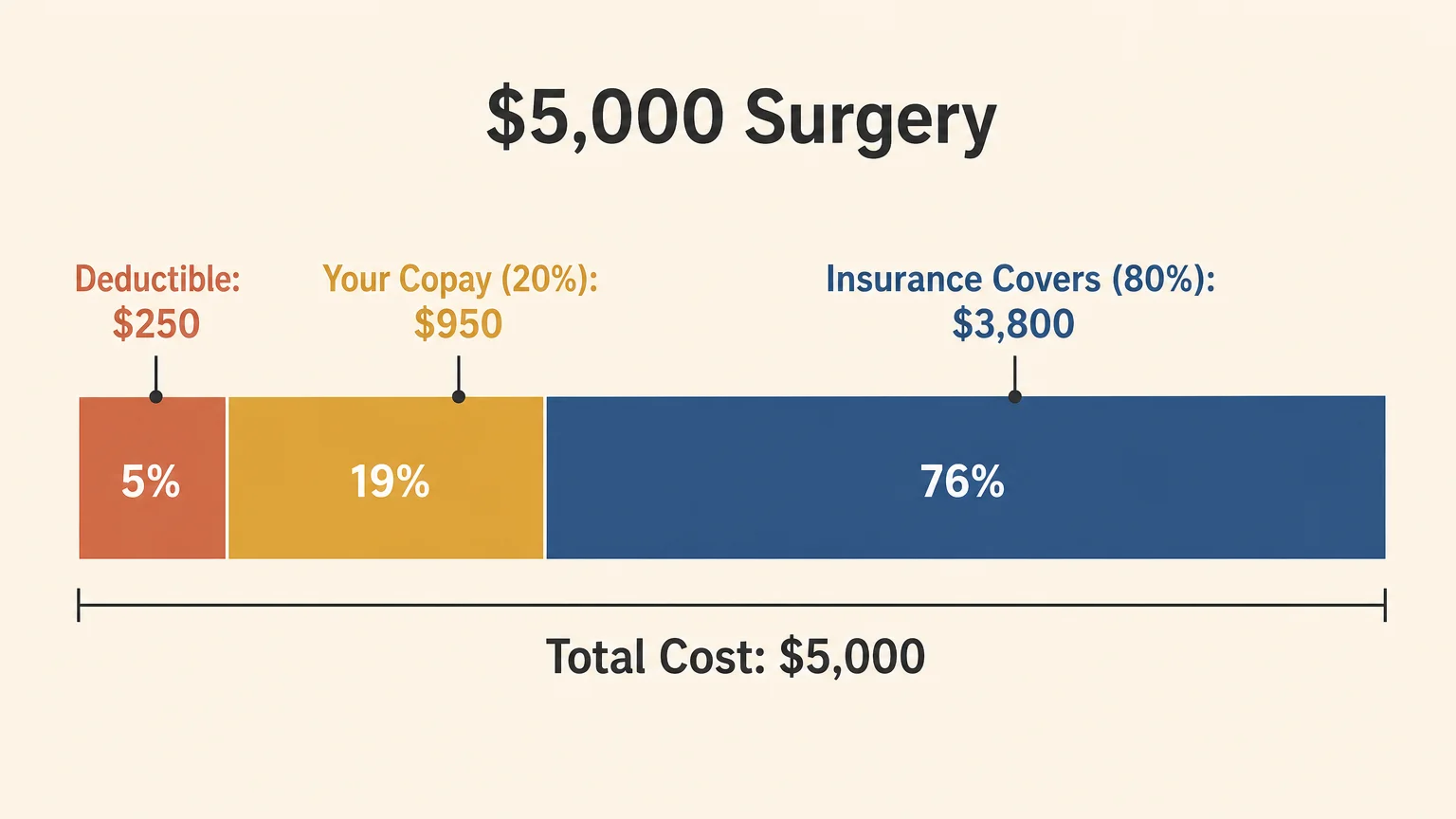

To understand why free pet insurance is structurally impossible for providers to sustain, you have to look at the raw economics of veterinary claims. Pet health insurance operates on a reimbursement model. You pay the veterinarian directly, submit your invoice, and the company reimburses you based on your coverage limits.

Because veterinary costs continue to rise, the premiums required to sustain these insurance pools must reflect the underlying risk. NAPHIA reports that in 2024, the average cost for a comprehensive accident and illness policy was roughly $62.44 per month for a dog and $32.21 per month for a cat. An accident-only policy, which covers broken bones and lacerations but ignores illnesses like diabetes or cancer, runs significantly cheaper—averaging around $16 per month for dogs and $9 per month for cats.

These averages serve as a baseline, but your actual quote depends entirely on your specific animal. Providers calculate premiums based on your zip code, the age of your companion animal, and their specific breed. A six-year-old French Bulldog living in Manhattan will command a drastically higher premium than a one-year-old mixed-breed cat living in rural Ohio. Recognizing these baseline costs helps you recalibrate your expectations. Instead of chasing non-existent free lifelong coverage, you can focus on adjusting deductibles and reimbursement rates to build a customized, affordable pet insurance plan that fits your exact budget.

Comparing Affordable Pet Insurance Plans vs. Alternatives

When weighing your options for veterinary financial protection, it helps to view the strategies side-by-side to understand the trade-offs between cost and coverage.

| Strategy | Average Monthly Cost | Best Used For | Major Limitations |

|---|---|---|---|

| 30-Day Free Trial | $0 | Newly adopted pets transitioning into a new home environment. | Expires after 30 days; does not cover pre-existing conditions prior to adoption. |

| Employer-Sponsored Plan | $0 to $40 (depending on corporate subsidy) | Working professionals seeking comprehensive, long-term coverage. | Tied directly to your employment; you may lose the group rate if you change jobs. |

| Standard Accident & Illness Policy | $32 (Cats) / $62 (Dogs) | Pet owners who want proactive protection against catastrophic bills. | Requires ongoing monthly payments; premiums generally increase as the pet ages. |

| Veterinary Discount Network | $10 to $15 | Routine care savings and pets with multiple pre-existing conditions. | Only covers a set percentage (usually 25%); you still pay the bulk of a major surgery. |

| Personal Emergency Savings | Determined by you | Disciplined savers who prefer self-insuring over paying monthly premiums. | Takes years to build; a major emergency early in the pet’s life will drain the fund instantly. |

Low-Cost Alternatives to Traditional Pet Insurance Plans

When standard insurance premiums fall completely outside your budget, you must build a robust alternative safety net. A variety of low-cost and subsidized options exist to help you manage sudden veterinary expenses without relying on traditional insurance models.

“While you cannot secure free lifelong insurance for your pet, the combination of 30-day trial certificates, employer-sponsored benefits, and charitable grants creates a patchwork safety net that functionally mimics free coverage during critical transition periods.”

First, look toward non-profit organizations and animal welfare charities. Groups like RedRover provide critical financial assistance when pet owners face an immediate, life-threatening medical crisis. Through the RedRover Relief Urgent Care grants program, qualified applicants can receive funding—typically around $250—to bridge the gap in emergency veterinary care. While $250 will not cover a massive surgery, it often covers the stabilization and diagnostic costs necessary to keep an animal alive while you arrange further financing.

Second, consider veterinary discount networks. These are not pet insurance plans. Instead, you pay a small membership fee, and participating veterinarians automatically deduct a set percentage from your medical services at checkout. There are no claim forms, no waiting periods, and no exclusions for pre-existing conditions. This makes them highly practical for older animals who are largely uninsurable.

Finally, medical credit options provide immediate liquidity. Financing tools like CareCredit allow you to pay for your pet’s emergency care immediately and spread the payments over several months. Many veterinary clinics partner with these lenders to offer promotional periods of deferred interest. If you pay the balance in full before the promotional period expires, you avoid the crushing interest rates entirely, turning a catastrophic upfront bill into manageable monthly installments.

Common Mistakes to Avoid

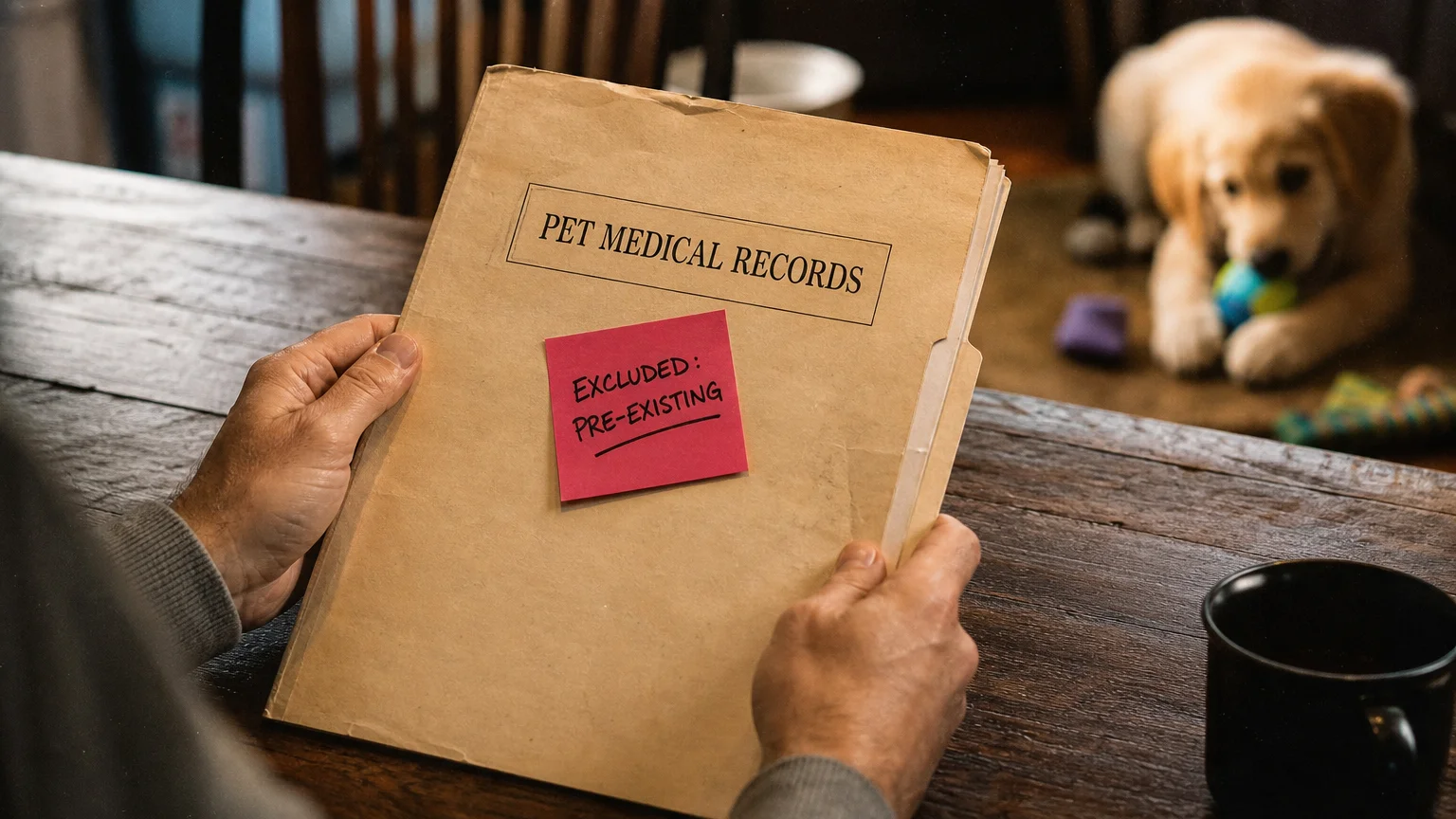

- Assuming Free Trials Cover Pre-Existing Conditions: If your newly adopted dog already has a noticeable limp or a documented ear infection at the shelter, the 30-day free trial will not cover the veterinary visit for that specific issue. Pet insurance strictly covers future, unpredictable events.

- Letting a Free Trial Lapse Unintentionally: Many pet owners activate a 30-day trial, place the paperwork in a drawer, and forget about it. If your pet experiences a severe emergency on day 35, you have zero coverage. You must actively choose a permanent plan before the promotional window closes.

- Confusing Discount Plans with True Insurance: Buying a $10-a-month veterinary discount card provides a helpful percentage off services at participating clinics. However, it will not reimburse you for an $8,000 emergency abdominal surgery the way true pet insurance coverage does. Understand exactly what financial product you are purchasing.

- Delaying Coverage Until Your Pet Gets Sick: Insurance relies on proactive enrollment. If you wait for a definitive cancer diagnosis or a broken leg to start shopping for affordable pet insurance, no company will cover the treatments related to those specific conditions.

Getting Expert Input

- Consult Your Primary Veterinarian: Before purchasing a policy or activating a promotional free trial, ask your local veterinary clinic which insurance companies they recommend. Clinic staff deal with claim reimbursements daily and can tell you which providers process payments quickly and which ones frequently deny valid claims.

- Speak with Your Human Resources Representative: If you suspect your employer offers pet health insurance, schedule a brief meeting with your benefits coordinator. Ask whether the company pays the full premium or simply offers a group discount rate, and verify if the coverage extends to pre-existing conditions under the corporate policy.

- Talk to a Financial Planner: If you are choosing between paying recurring monthly pet insurance premiums or building a dedicated high-yield savings account for pet emergencies, a financial expert can help you weigh the opportunity costs. They can analyze your discretionary income and help you determine which risk-management strategy best protects your overall financial health.

Frequently Asked Questions

Does the ASPCA offer free pet insurance?

No, the ASPCA pet health insurance program is a paid consumer product managed by a third-party provider. They do not offer free lifelong coverage, though you may occasionally find promotional trial periods offered through specific shelter partnerships.

Can I get pet insurance for free if I receive government assistance?

Traditional pet insurance companies do not offer free or subsidized policies based on human income levels. However, many local humane societies and state-level animal charities run subsidized clinics that provide heavily discounted or free veterinary care for individuals facing severe financial hardship.

Are 30-day free pet insurance trials actually worth activating?

Absolutely. Puppies, kittens, and newly adopted adult dogs are highly prone to contracting minor infections in a new environment or experiencing stress-related gastrointestinal issues. Activating a trial gives you an immediate financial safety net during this high-risk transition period without requiring a long-term financial commitment.

Protecting your animal from medical emergencies does not always require signing up for an expensive lifelong policy. By taking advantage of 30-day promotional trials, investigating your employer benefits, and familiarizing yourself with charitable grants and discount programs, you can strategically shield yourself from devastating veterinary bills. Make proactive choices today so that if an emergency strikes tomorrow, your focus remains entirely on your pet’s recovery rather than your bank account.

This is general informational content based on widely accepted guidance. Individual results vary. Verify current details—rules, prices, eligibility, regulations—with official sources before making important decisions.

Last updated: June 2026. Rules, prices, and details change—verify current information with official sources before acting on it.