Adding a pet to your retirement plan is one of the most rewarding decisions you can make, offering daily companionship, lower blood pressure, and a built-in routine. Transitioning to a pet-friendly lifestyle requires a clear understanding of the financial and logistical realities of modern pet ownership. While a dog or cat can reduce stress and prevent isolation, the commitment stretches beyond daily walks and extra cuddles. From navigating the rising costs of veterinary care to legally planning for your animal’s future, bringing a pet into your home is a major life change. By evaluating your retirement budget, travel goals, and daily energy levels, you can successfully find the perfect animal companion to share your golden years.

1. The Real Cost of a “Free” Pet

Many retirees assume that once the mortgage is paid off and daily commuting costs vanish, their fixed income will easily absorb the cost of an animal. However, the financial realities of modern pet ownership might surprise you. While the initial adoption fee for a rescue animal might be minimal, the lifelong financial commitment is substantial. The percentage of pet owners in the U.S. has spiked over the past three decades, with 66% of households now owning a pet. Along with that surge in ownership, the associated costs have dramatically increased.

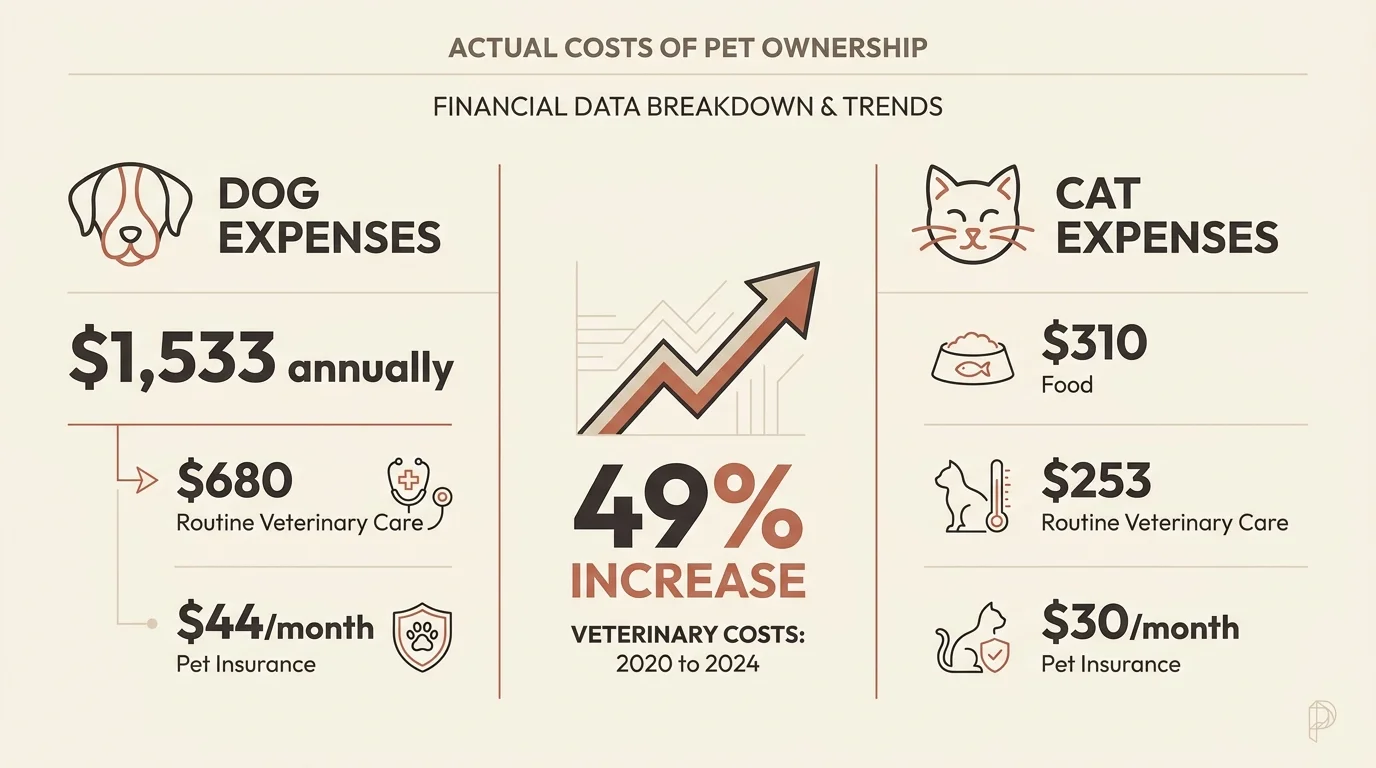

According to Forbes Advisor, essential dog expenses currently cost an average of $1,533 annually. That figure represents just the baseline for a healthy animal. Routine veterinary care alone accounts for approximately $680 of that total. Cat owners face slightly lower, but still significant, expenses, typically spending about $310 on food and $253 on routine veterinary care each year. Furthermore, the American Pet Products Association reported that the overall cost of pet ownership skyrocketed by 49% between 2020 and 2024, driven largely by inflation in veterinary care, prescription diets, and specialized medications.

If you are living on a fixed retirement income, one unexpected medical emergency can easily derail your monthly budget. A single surgery for a swallowed toy or an unexpected cancer diagnosis can cost thousands of dollars out of pocket. To mitigate this risk, many retirees are turning to pet insurance. Comprehensive insurance plans can act as a financial safety net, costing an average of $44 a month for dogs and $30 a month for cats. When calculating whether a pet fits into your retirement plan, you must factor in these modern inflation rates rather than relying on what pet care cost twenty years ago.

2. Energy Matching is More Important Than Breed

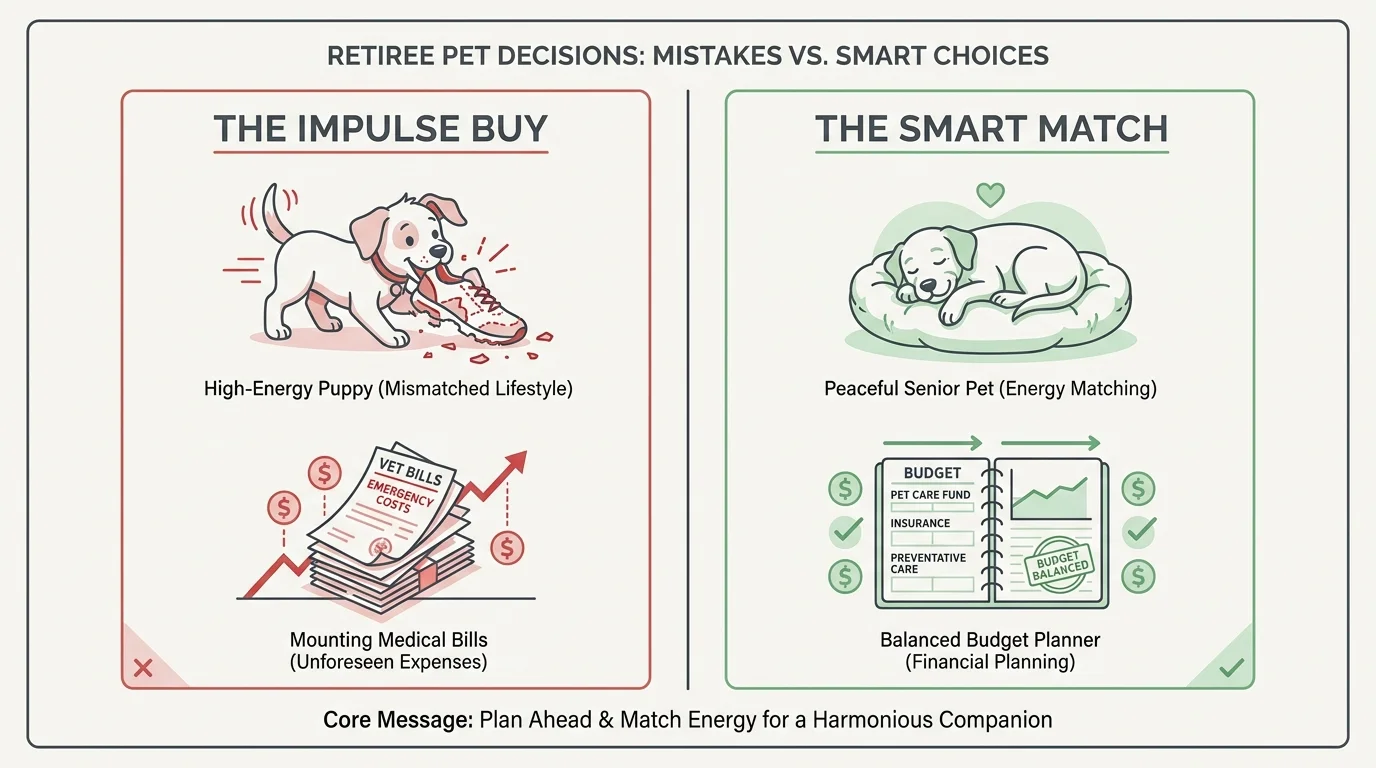

Puppies and kittens are undeniably charming, but they demand a monumental amount of physical and emotional endurance. Housebreaking, obedience training, boundary testing, and middle-of-the-night bathroom trips can quickly disrupt the peaceful retirement schedule you worked so hard to achieve. Instead of defaulting to a young animal or a specific breed you remember fondly from your childhood, focus on matching an animal’s current energy level to your daily physical capabilities.

Physical limitations sometimes accompany aging, and an energetic, pulling 70-pound Labrador Retriever poses a very real fall risk on an icy sidewalk. This is exactly why animal welfare advocates strongly encourage older adults to consider senior pets. Shelters across the country facilitate “Seniors for Seniors” programs, which deeply discount or entirely waive adoption fees for older adults willing to take in a mature pet. Senior animals are typically housebroken, well past the destructive chewing phase, and perfectly content to spend their afternoons napping on a sunlit rug.

If you prefer a specific type of companion, consider breeds and species recognized for their low-maintenance lifestyles:

- Senior Cats: Felines make perfect companions for a quieter retirement. They offer cozy company, require no outdoor leash walking, and provide soothing purrs that many find exceptionally calming.

- Dachshunds: Known for their devoted nature, these small dogs fit well into varying schedules, require minimal grooming, and are generally satisfied with a moderate 30-minute daily walk.

- Boston Terriers: Alert but naturally laid-back, these dogs make wonderful companions for those who want a friendly presence in their home without the demand for marathon running or intense hiking.

3. Your Travel Plans Might Need a New Itinerary

Retirement often brings the freedom to pack up and travel at a moment’s notice. Whether you plan to spend winters in a warmer climate, take extended international cruises, or frequently visit family across the country, a pet immediately changes your logistical landscape. You can no longer lock the front door and head to the airport; your travel plans must now account for your animal’s well-being.

If you plan to leave your pet behind, professional care is expensive. A standard seven-day vacation will cost an average of $253 just for dog boarding facilities. If you travel multiple times a year, those boarding fees compound rapidly. Alternatively, hiring an in-home pet sitter allows your animal to remain in a familiar environment, but it requires coordinating schedules and trusting a professional with access to your home.

If you intend to bring your pet along for the ride, you must navigate an entirely different set of hurdles. Airlines enforce strict regulations regarding the size of in-cabin pet carriers, and traveling with a larger dog often means expensive cargo fees or long road trips. Additionally, crossing international borders—and even traveling to certain states like Hawaii—requires up-to-date health certificates, specific vaccinations, and occasionally mandatory quarantine periods.

| Pet Care Option During Travel | Estimated Financial Cost | Best Suited For | Potential Drawbacks |

|---|---|---|---|

| Professional Boarding Facility | $35 to $70+ per night | Highly social dogs that require constant supervision | Can be loud and stressful for anxious or older pets |

| In-Home Professional Pet Sitter | $50 to $100+ per night | Cats, senior dogs, and multi-pet households | Requires finding and trusting a stranger in your house |

| Traveling With Your Pet | Variable (airline fees, hotel pet deposits) | Adaptable, small dogs or highly leash-trained cats | Strict TSA rules, limited itinerary flexibility, and added travel stress |

4. Fostering Might Be Your Perfect Middle Ground

If you want the companionship and routine of an animal without a rigid ten-to-fifteen-year commitment, fostering is a brilliant alternative. Local rescues and municipal animal shelters desperately need safe, quiet homes for animals recovering from surgery, awaiting permanent placement, or simply needing a temporary break from the chaotic shelter environment.

Fostering removes almost all the financial barriers to having a pet in your home. The rescue organization typically covers all veterinary expenses, prescribed medications, and often provides the necessary food and supplies. Your primary responsibility is to offer a loving environment, basic training, and daily care.

This arrangement is particularly beneficial for retirees who plan to travel for part of the year. You can foster a dog or cat for a few months during the summer, help them find their forever home, and then travel freely during the winter months without worrying about boarding fees. Furthermore, fostering serves as an excellent trial period. It allows you to evaluate how an animal actually fits into your daily retirement routine before you make a permanent, legal commitment to adoption.

5. Pet Trusts Are Legal, Real, and Necessary

One of the most difficult realities of adopting a pet later in life is the possibility that your animal companion might outlive you. Relying on a casual handshake agreement with a family member or neighbor is a deeply flawed strategy. Far too often, relatives are either unwilling or financially unable to take on the burden of a pet, resulting in heartbroken older animals being surrendered to overcrowded shelters.

To prevent this, you need a formal legal strategy. Thanks to growing awareness of the human-animal bond, all 50 states and the District of Columbia have passed legislation allowing for the creation of companion animal trusts. The Uniform Probate Code and the Uniform Trust Code provide the legal foundation for these documents, ensuring your wishes are honored.

According to the American Bar Association, a pet trust is a legally sanctioned tool that creates a fiduciary obligation to care for your animal. Unlike a traditional will—which considers pets as property and must slog through a lengthy probate process—a pet trust takes effect immediately upon your death or severe incapacitation. You officially designate a trusted caregiver, appoint a separate trustee to manage the funds, and leave behind specific financial resources dedicated exclusively to your pet’s veterinary care, grooming, and daily diet. This ensures your pet’s standard of living never drops, no matter what happens to you.

Common Mistakes to Avoid

Even with the best intentions, retirees can easily fall into a few predictable traps when bringing a new pet home. By recognizing these pitfalls early, you can protect both your finances and your peace of mind.

- Underestimating veterinary inflation: Assuming that your new dog’s healthcare will cost the same as the dog you owned in the 1990s is a recipe for budget disaster. Veterinary medicine now utilizes advanced diagnostics, MRI machines, and specialized oncology treatments, all of which carry premium price tags.

- Choosing nostalgia over practicality: You may have fond memories of hiking with a high-energy working breed, like a Border Collie or an Australian Shepherd, during your thirties. However, adopting a high-drive working dog when your current lifestyle favors reading and gardening will result in a frustrated animal and an exhausted owner.

- Assuming your adult children will adopt the pet: Never assume your children or grandchildren will automatically take your pet if you move into assisted living. They have their own jobs, housing restrictions, and financial burdens. Always secure a backup plan in writing.

- Skipping pet insurance to save a few dollars: Passing on a $40 monthly premium might seem like smart savings until you are handed a $5,000 estimate for emergency orthopedic surgery. Insurance protects your retirement nest egg from sudden, catastrophic veterinary bills.

Getting Expert Input

Because bringing an animal into your life intersects with your physical health, your finances, and your estate plan, it pays to seek professional guidance before heading to the shelter.

- Consult a Veterinarian: Before adopting, schedule a brief consultation with a local vet. Ask them about the typical lifetime medical costs of the specific breed you are considering and what common ailments you should expect as the animal ages.

- Speak with a Financial Advisor: Ask your financial planner to help you carve out a realistic pet care “sinking fund” from your retirement distributions. Stress-test your budget against the potential for high out-of-pocket medical emergencies.

- Hire an Estate Planning Attorney: Do not attempt to draft a pet trust on a scrap of paper. Work with a qualified attorney to formally integrate a legally binding pet trust into your broader estate plan, ensuring the document complies with the specific trust laws of your state.

Frequently Asked Questions

Are there specific adoption programs for senior citizens?

Yes, many animal rescues and municipal shelters offer “Seniors for Seniors” programs. These community initiatives typically discount or entirely waive standard adoption fees for older adults who choose to open their homes to a mature dog or cat.

Does Medicare cover any costs for a service dog or emotional support animal?

No. Original Medicare and Medicare Advantage plans do not cover the purchase, specialized training, food, or veterinary care of service dogs or emotional support animals. You are entirely responsible for the financial upkeep of your pet.

How much should a retiree budget annually for a dog?

Based on recent industry data, you should budget a minimum of $1,500 annually for essential dog expenses like food, routine vaccinations, and preventative medications. However, unexpected medical emergencies can easily double or triple that amount if you do not carry pet insurance.

Adding an animal companion to your life brings immeasurable joy, laughter, and comfort to your retirement years. By approaching pet ownership with clear eyes about the financial, physical, and legal responsibilities, you ensure a wonderful, stress-free experience for both you and your new best friend.

This article provides general information only. Every reader’s situation is different—what works for others may not be the right fit for you. For personalized guidance on health, legal, or financial matters, consult a qualified professional.

Last updated: May 2026. Rules, prices, and details change—verify current information with official sources before acting on it.